| 作者 |

美国是否应该放弃U.S. GAAP, 而采用IFRS会计准则? 美国是否应该放弃U.S. GAAP, 而采用IFRS会计准则? |

|

抢注G8

[博客]

头衔: 海归中校

声望: 教授

性别:

加入时间: 2007/02/17

文章: 836

来自: 苏州

海归分: 52976

|

|

|

作者:抢注G8 在 海归商务 发贴, 来自【海归网】 http://www.haiguinet.com

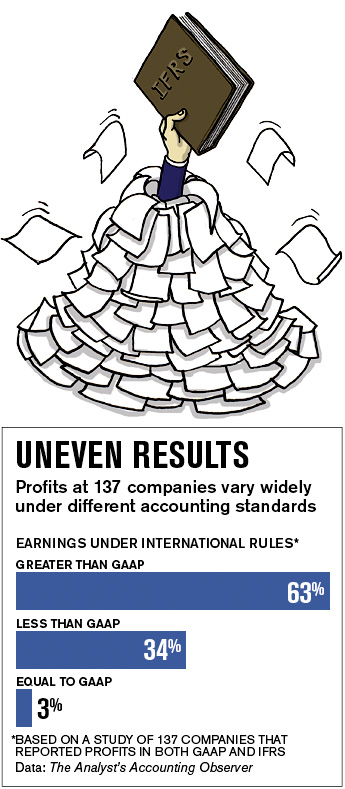

【自2007年11月起,美国SEC容许在美国上市的外国公司使用International Financial Reporting Standards (IFRS), 提交各种财务申报。但是,业界对此反应不一,一方面担心标准不同,不能在一个基本面上进行财务比较,影响投资者的分析;另一方面,认为U.S. principles 多达25,000页,繁琐,复杂,而IFRS只有2,500页,比较简洁和明了。根据 The Analyst's Accounting Observer 对137家上市公司的利润报表用GAAP和IFRS比较,结果发现63%的公司显示IFRS利润高出GAAP;34%低于GAAP, 3%与GAAP 吻合。

在欧洲,只有英国很少有Off-Balance-Sheet entities。目前29个国家采用IFRS,但是都有一些根据本国实际情况的修改。因此,即使号称为International, 也很难做到完全一样,每个国家和地区在执行上也有差异,隐藏着很多不确定因素和差异。】

Businessweek: News September 4, 2008, 5:00PM EST text size: TT

Global Accounting Rules: Simpler, Yes. But Better?

Dumping GAAP could ease the burden on some companies, but adopting the streamlined British model has its pitfalls

by David Henry

In the latest example of the waning financial leadership of the U.S., the Securities & Exchange Commission wants to dump the country's complex accounting rules in favor of a simpler set of international principles. It's a major step toward a single worldwide standard—a necessity for creating seamless global markets. But adopting the model, which is relatively new and untested, has its own pitfalls.

Junking the U.S. rules, known as generally accepted accounting principles, or GAAP, would have seemed preposterous a decade ago. Back then investors and companies, both in the U.S. and worldwide, viewed GAAP as the gold standard, a transparent system for reporting earnings and other financials. As more European and Asian companies rolled out results in the American style as well as their own, it seemed GAAP would be the top choice among bean counters in an increasingly global marketplace.

But GAAP has gotten so unwieldy that it has all but collapsed under its own weight. According to accounting firm PricewaterhouseCoopers, the U.S. principles span 25,000 pages, compared with 2,500 pages of the International Financial Reporting Standards (IFRS), the ones the SEC is promoting. Navigating that maze, say critics, is costly and confusing. "We've got something that's suited to a different era, that's not global," says Robert H. Herz, chairman of the Financial Accounting Standards Board, the body that oversees GAAP. "I believe it's better to create something new than to patch up something old and outdated."

Assuming certain improvements are made to the international standards, U.S. public companies would switch over by 2016. The change, which some large outfits could make as early as 2010, would create a common accounting regime, ideally allowing investors to compare a Silicon Valley technology company with one in Germany or Japan. Companies also could better analyze cross-border acquisition opportunities, says William T. Keevan, a forensic accountant and director at consultant SRA International and at for-profit school DeVry. And it would be a boon for accounting firms, which will guide companies through the new system—not unlike the frenzy of activity for technology firms leading up to Y2K. "One of the more revolutionary developments in the world's capital markets is the quickening pace of acceptance of a true lingua franca for accounting," SEC Chairman Christopher Cox said in late August.

But even if companies are speaking the same language, their financial stories may be decidedly different from each other. That's because, compared with GAAP's detailed requirements, the international principles tend to be broad, giving companies wiggle room. GAAP, for example, contains more than 200 rules for recording revenue, while IFRS only has a couple of requirements. "Basically, you can do almost anything you want," says Herz.

In the end, that can lead to wide variances in profit reporting. A study by Jack T. Ciesielski of The Analyst's Accounting Observer found that, among the 137 companies reporting 2006 results under both GAAP and IFRS, 63% showed higher earnings with the international standards. For the median company, profits jumped by 11%.

Even under one system, enforcement and cultural interpretations of the international rules can vary by country. For instance, although British companies rarely employ off-balance-sheet entities, the vehicles crop up elsewhere in Europe. And an estimated 29 countries that use IFRS have added their own exceptions to the rules, defeating the purpose of a global standard. "We may get something that people think is uniform but is not," says Lawrence A. Cunningham, a law professor at George Washington University. "There is a real risk of a veneer of comparability that hides a lot of differences."

Henry is a senior writer at BusinessWeek.

[url]

[/url][img]https://files.haiguinet.com/flashupload/UploadedFiles/1220903211_394picture.jpg" border="0" title="click to view fullsize image"/>

作者:抢注G8 在 海归商务 发贴, 来自【海归网】 http://www.haiguinet.com

|

|

|

| 返回顶端 |

|

|

|

-

美国是否应该放弃U.S. GAAP, 而采用IFRS会计准则? -- 抢注G8 - (4858 Byte) 2008-9-09 周二, 03:43 (1860 reads) 美国是否应该放弃U.S. GAAP, 而采用IFRS会计准则? -- 抢注G8 - (4858 Byte) 2008-9-09 周二, 03:43 (1860 reads)

|

|

|

|

您不能在本论坛发表新主题, 不能回复主题, 不能编辑自己的文章, 不能删除自己的文章, 不能发表投票, 您 不可以 发表活动帖子在本论坛, 不能添加附件不能下载文件, |

|

|